As DN writes, ART was down close to 10% in February, which is quite normal for us. It's hard enough to deliver 20-30% returns annualized, if it's not to be without volatility. What struck us in this regard was how much pessimism was out there.

This is not meant to be any criticism of Dagens Næringsliv, but a general comment that there is information in the amount of negativity in the financial press.

The market and the news picture rarely go hand in hand

To take the elementary first: Bottoms in the market do not coincide with good news, but with bad news. This fairly obvious truth is hard to keep in mind when it storms and one is more easily depressed because the portfolio has fallen in value. Sentiment follows prices, not the other way around. If anything, one should rather look at the possibility of increasing risk in their portfolio when sentiment is so poor and we think the market going forward will definitely overash on the upside.

The reason for much of the uncertainty in the market, and the gloomy headlines, can of course be summed up to Donald Trump, and primarily what is simply tax and levy policy. The concerns are mainly that the introduction of (increased) tariffs will increase inflation, which could lead to increased interest rates, as well as over time reduce free trade which, at the margin, will be a persistent negative factor on global growth.

Trump as explanation -- or apology?

There is, however, grounds to believe that the fears are fried excessively, and possible the market turmoil has less to do with Trump than the headlines would suggest.

Firstly the market has had time to price in and businesses have had time to adjust to Trump's tariffs at least since November. Possibly some were of the opinion that this was a negotiating outcome (it still may be), which would not be carried out (obviously not the case).

Secondly traders, where imports are a major part of their business, have run ahead of increased tariffs and replenished their stocks. This is visible in the import data. Therefore, it will be quite natural if activity weakens in the coming months. It's not necessarily a sign of recession or some kind of lasting new condition.

https://fred.stlouisfed.org/graph/fredgraph.png?g=1FHZh&height=490

Thirdly The tariff increase introduced under Trump 1.0 (and extended under Biden) did not result in any significant increase in inflation. There is, of course, a high probability of seeing a one-time effect of the tariff increase when it is introduced, but not necessarily one-to-one with the tax increases. In the event of one-off effects, inflation will return to zero at the next measurement, thus something that central banks and the market see through.

https://fred.stlouisfed.org/graph/fredgraph.png?g=1FHZT&height=490

Fourthly: could it be that the correction we've seen had little to do with Trump policies, but driven by other factors? A correction of the magnitude seen in February-March 2025 is a relatively common occurrence, and not something that should cause panic.

Liquidity drives the market more than politics

In addition, we saw a sharp increase in the dollar exchange rate and US interest rates in the fourth quarter. Purely overall, stronger dollar yields less global liquidity, making stronger dollar = weaker risk assets (with a lag)

Raoul Pal and Julien Bittel have published a lot of work on the subject in the Macro Investing Tool and Global Macro Investor, and the accuracy of this has so far been striking.

Now that the dollar has weakened, and US 10-year interest rates have fallen 0.6% in two months, this headwind will turn into tailwinds as we enter the second quarter.

The weakening of the dollar has also increased the room for action of the Chinese, and in the aftermath of the party congress, a major package of measures was announced in mid-March.

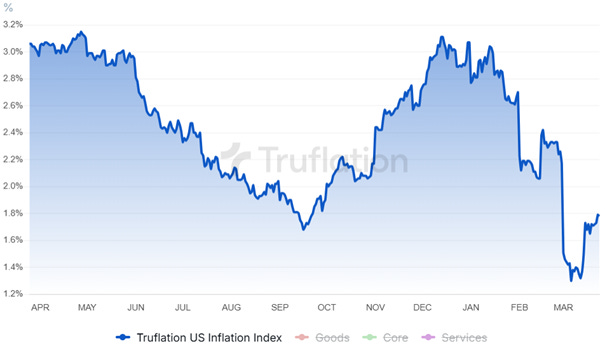

In addition to this, there is little evidence that inflation is increasing, at least if Truflation is to be believed which fetches tens of thousands of prices from the web continuously. This should ensure that the US central bank (Fed) is not going to stick sticks in its wheels. After all, the Fed recently announced a phase-out of its bond sales that will in effect provide more liquidity, and a push upward to the equity and crypto markets.

Risk always exists, but it is rarely the risk that “everyone” worries about that is something to fear. In 2016, the consensus expectation, both with strategists and in the media, was that a Trump victory would be disastrous for stock markets. The fact became something completely different. With all the tailwinds that are in store, a good likelihood is that we will now have a repeat of the phenomenon, and we find no reason to position ourselves for anything other than the path of least resistance being up at the moment.

Who is shouting "bubble"? And why memory, of all things?

Micron has skyrocketed. So have SK Hynix and Samsung's memory division. And as if on cue, a host of people have appeared on X, in comment sections, and during coffee breaks who have found their new favorite word: bubble. Let's pause there for a moment.

Asymmetri som strategi

Symmetri signaliserer god helse, stabile gener, fravær av utviklingsforstyrrelser. Det er en evolusjonær snarvei: hjernen vår tolker symmetri som “alt er på stell”. I investeringer er det stikk motsatt; der er asymmetri det du burde leter etter.

Infinite supply

What happens when machines take over human labor? In 2022, what has subsequently been called “The Chat-GPT moment” occurred. In 2026, we will have what will eventually be called “The OpenClaw moment”.

{kind=link}

{kind=link}